Buying a home is a big step, and getting a mortgage can feel confusing, especially if you’re new to the process. Today, many banks and lenders let you get mortgage pre approval online, which can save you time and give you an advantage when making an offer on a house. Here’s a practical guide to understanding how online pre-approval works, what you need to prepare, and how to avoid common mistakes.

What Is Mortgage Pre Approval?

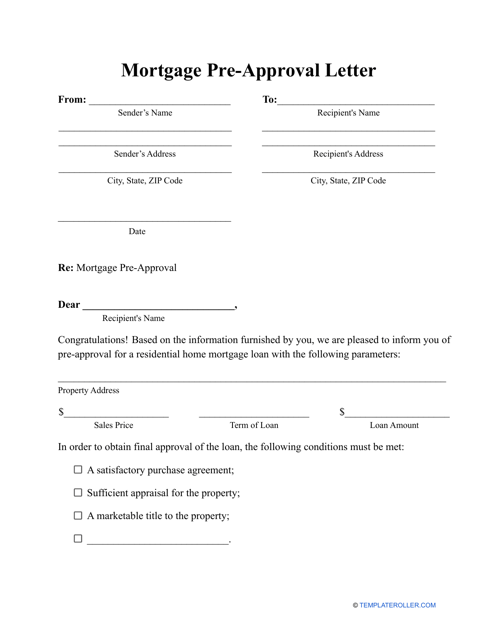

A mortgage pre approval is a letter from a lender showing how much money you’re likely to borrow for a home loan. It’s not a final offer, but it tells sellers you’re a serious buyer. Online pre-approval lets you do this from home—no need to visit a bank in person.

With pre-approval, you’ll know your price range before you start house hunting. Sellers often prefer buyers with pre-approval, because it means fewer surprises during the sale.

How Online Pre Approval Works

Getting pre-approved online is usually fast and straightforward. Most lenders have simple forms on their websites. Here’s how the process typically goes:

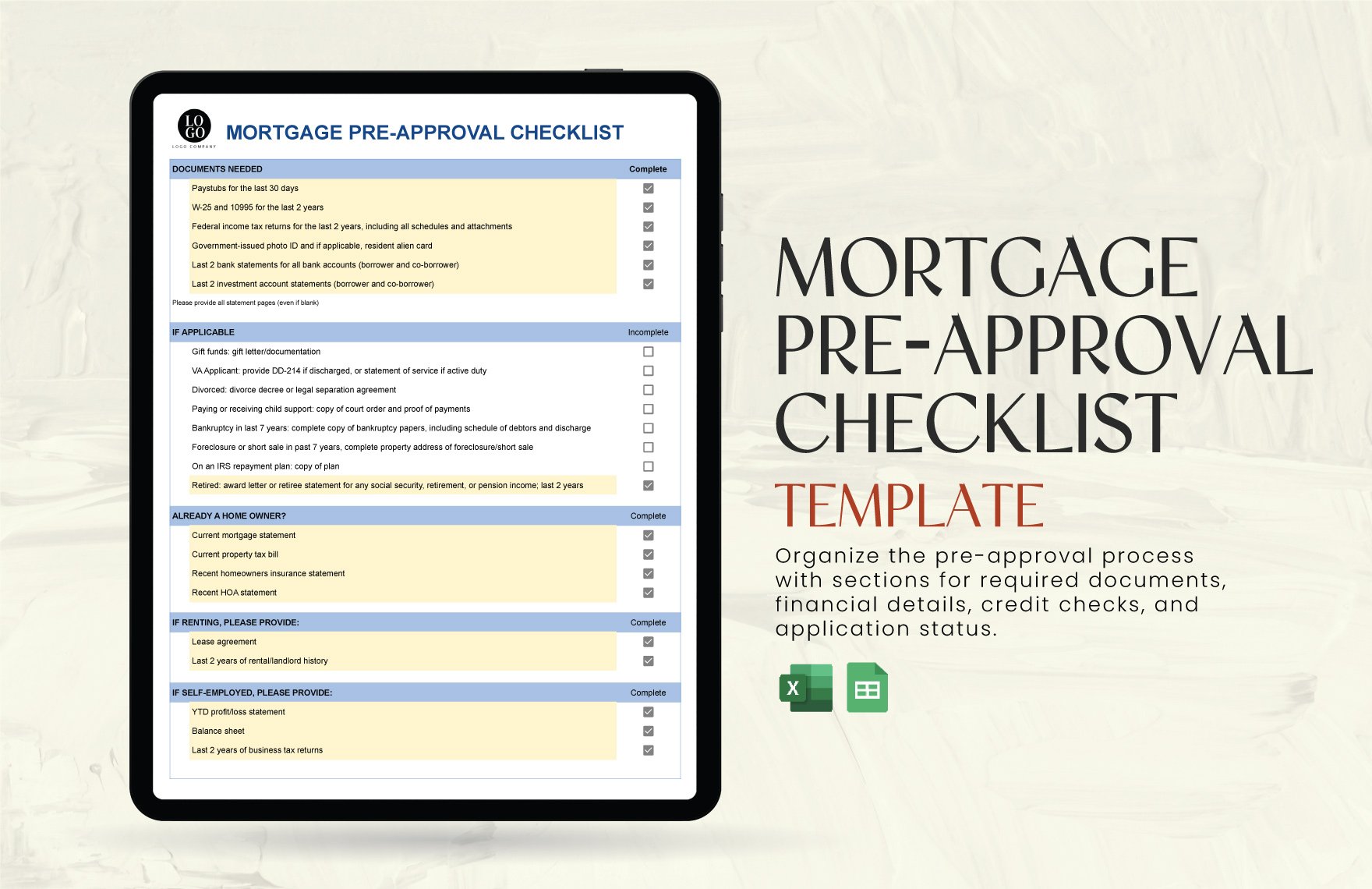

- Fill out an application: You enter personal information, income, debts, and the type of property you want.

- Submit documents: You’ll upload things like pay stubs, bank statements, or tax returns.

- Credit check: The lender checks your credit score and history.

- Get your pre-approval letter: If you qualify, you’ll get a letter stating how much you can borrow.

The whole process can take just a few hours, but sometimes up to a few days if extra documents are needed.

Key Requirements

- Good credit score (usually 620 or higher)

- Stable income

- Low debt-to-income ratio (typically below 43%)

- Proof of assets (savings, investments)

Benefits Of Getting Pre Approved Online

Online pre-approval offers several advantages over the traditional in-person approach:

- Convenience: Apply anytime, anywhere.

- Speed: Many online applications take less than 20 minutes.

- Faster home shopping: You’ll know your budget right away.

- Stronger offers: Sellers often accept offers with pre-approval letters more quickly.

Many lenders use secure websites to keep your information safe. However, always check that the site uses “https” in the address and is a trusted brand.

Comparing Online Lenders

Not all online lenders are equal. Here’s a simple comparison of three popular online lenders for pre-approval:

| Lender | Minimum Credit Score | Typical Approval Time | Application Fee |

|---|---|---|---|

| Rocket Mortgage | 620 | Within 1 day | None |

| Better.com | 620 | Same day | None |

| Bank of America | 620 | 1-3 days | None |

Always read reviews and check customer service options. Some online-only lenders may not offer face-to-face help, which can be tricky for first-time buyers.

Step-by-step: Getting Mortgage Pre Approval Online

Let’s break down the process into clear steps:

- Research lenders. Find a few online lenders with strong ratings and clear information.

- Gather documents. Collect your ID, pay stubs, tax returns, bank statements, and any other required paperwork.

- Check your credit. Fix any mistakes before applying, as your credit score affects your offer.

- Complete the online application. Enter accurate information.

- Upload documents securely. Use the lender’s online portal.

- Wait for a decision. Most lenders reply within 24–72 hours.

- Download your pre-approval letter. Keep it handy for your agent and sellers.

Common Mistakes To Avoid

- Guessing your income or debts—always be accurate.

- Applying to too many lenders at once, which can hurt your credit.

- Not checking if your pre-approval has an expiration date (usually 60–90 days).

What Lenders Look For

Lenders focus on a few main factors when reviewing your online application:

| Factor | Why It Matters | Typical Requirement |

|---|---|---|

| Credit Score | Measures your risk as a borrower | 620 or higher |

| Debt-to-Income Ratio | Checks if you can afford new payments | Below 43% |

| Proof of Income | Ensures you have steady earnings | 2 years of work history |

| Assets | Shows you have enough for a down payment | Bank statements or investment accounts |

If you’re self-employed, expect to share extra documents like business tax returns.

Non-obvious Insights

Many first-time buyers think pre-approval is a guarantee. It’s not. Lenders can still deny your loan if your finances change or the home doesn’t appraise for enough value. So, avoid making big purchases or taking on new debt between pre-approval and closing.

Another detail: pre-approval letters may be for the maximum you can borrow, but you don’t have to spend that much. Stay within a budget you’re comfortable with, considering property taxes, insurance, and repairs.

Is Online Pre Approval Right For You?

Online pre-approval is best if you want a fast, simple way to start your home search. It’s also ideal if you’re comfortable using technology and uploading documents. However, if you have a complicated financial history or need lots of guidance, you might prefer a lender with strong phone or in-person support.

Before choosing, compare rates and fees. Even small differences can cost thousands over the life of your loan. For detailed comparisons, see resources like Consumer Financial Protection Bureau.

Frequently Asked Questions

How Long Does Online Mortgage Pre Approval Take?

Most online lenders give you a decision within 24 to 72 hours, if you upload all documents quickly. Some can respond in minutes if your information is easy to verify.

Does Getting Pre-approved Online Hurt My Credit Score?

Yes, but only a little. Lenders do a “hard inquiry” on your credit, which usually lowers your score by a few points. Multiple inquiries within a short period (45 days) usually count as one.

Can I Get Pre-approved If I’m Self-employed?

Yes, but you’ll need extra paperwork. This usually means two years of business tax returns and proof of consistent income.

Is Pre-approval The Same As Final Loan Approval?

No. Pre-approval means you’re likely to qualify based on what you shared. Final approval happens after you choose a home, get an appraisal, and the lender checks everything again.

How Long Does A Pre-approval Letter Last?

Most letters are valid for 60 to 90 days. If you don’t find a home in that time, you’ll need to update your information and get a new letter.

Getting mortgage pre approval online is a smart first move when buying a home. It gives you confidence, speeds up your search, and shows sellers you’re ready. Just remember to compare lenders, prepare your documents, and use your pre-approval wisely. With a little planning, you’ll be well on your way to owning your next home.

Read More:

- Affordable Life Insurance Policy: Secure Your Future Without Breaking the Bank

- Business Liability Insurance Quote: Get the Best Rates Today

- Private Health Insurance Plans: Top Benefits and How to Choose

- Best Car Insurance Quotes Online: Save Big With Top Rates

- Compare Home Insurance Rates: Save Money With Smart Choices

- Best Personal Loan Rates: Unlock Top Offers for 2024

- Small Business Loan Pre Approval: Unlock Funding Faster

- Debt Consolidation Loan Online: Simplify Your Finances Today