Affordable Life Insurance Policy: Your Guide To Smart, Low-cost Coverage

Life is full of surprises. Some are happy, like a new baby or a new home. Others are hard to face, like losing someone you love. That’s why many people look for affordable life insurance—it helps protect your family if something happens to you, without costing too much each month.

But what does “affordable” really mean? Is cheap always better? How do you find a policy that gives enough protection, but doesn’t break your budget? If you are new to life insurance, the choices can feel confusing. This article will explain everything you need to know about getting affordable life insurance, so you can make a confident decision for your family’s future.

What Is Affordable Life Insurance?

When people talk about affordable life insurance, they usually mean term life insurance. This type of policy is simple and low-cost. You pay a fixed amount each month (called a premium). If you die during the term, your family gets a payout (called a death benefit). If you outlive the term, the policy ends and you don’t get your money back.

Affordable life insurance is not about finding the absolute cheapest plan. It’s about balancing cost and coverage. The goal is to get enough protection for your family—so they can pay for things like the mortgage, college, or daily bills—without spending more than you can handle.

Why Life Insurance Matters

Some people think life insurance is only for older people or those with children. In reality, almost anyone can benefit. Here are a few reasons why:

- Family protection: If you support your spouse, children, or parents, life insurance helps them cover living expenses if you die.

- Debt coverage: Your debts (like a mortgage or student loans) don’t always disappear when you die. Insurance can cover these costs.

- Peace of mind: Knowing your family will be okay financially can reduce stress.

- Affordable rates: The younger and healthier you are when you buy, the lower your monthly cost.

Types Of Affordable Life Insurance Policies

There are many types of life insurance, but only a few are truly affordable for most people. Understanding the main options can help you choose wisely.

| Policy Type | Typical Cost | Coverage Length | Main Benefit |

|---|---|---|---|

| Term Life | Low | 10–30 years | Simple, fixed cost |

| Whole Life | High | Lifetime | Builds cash value |

| Group Life | Very Low | As long as employed | Offered by employers |

| No-Exam Term | Medium | 10–30 years | Quick approval |

Term Life Insurance

This is the most popular affordable life insurance. You pick how long you want coverage (usually 10, 20, or 30 years), and your premium stays the same. If you die during the term, your loved ones get money. If not, the policy ends.

Why choose it: It’s simple, easy to understand, and costs much less than other types. Many young families and new homeowners choose term life.

Group Life Insurance

Many employers offer a small amount of life insurance for free or at a very low cost. This is called group life insurance. It’s easy to get, but the coverage is usually not enough to fully protect your family. Also, you lose it if you change jobs.

Why choose it: It’s a good start, but you may need extra coverage on your own.

No-exam Life Insurance

Some policies don’t require a medical exam. This means you can get approved faster, but the price is usually higher. It’s best for people who need life insurance quickly or have health problems.

Why choose it: If you need insurance right away or can’t qualify for regular term life, this can be a good option.

Whole Life Insurance

Whole life insurance covers you for your entire life, and it builds up cash value you can borrow against. However, it costs much more—often 5–10 times more—than term life. Most people looking for affordable life insurance choose term, not whole life.

Why choose it: Only if you need lifelong coverage and can afford higher premiums.

How Much Life Insurance Do You Need?

Choosing the right amount is key to finding an affordable policy. Too little, and your family may struggle. Too much, and you pay for coverage you don’t need.

A simple rule is the 10-12 times rule: Buy coverage equal to 10–12 times your yearly income. For example, if you earn $40,000 per year, aim for $400,000–$480,000 in coverage.

But everyone’s situation is different. Consider:

- Your annual income and how long your family would need it replaced

- Large debts (mortgage, loans, credit cards)

- Children’s education costs

- Final expenses (funeral, medical bills)

A more detailed way is to add up all the costs your family would face, then subtract any savings or other life insurance you already have.

What Affects The Cost Of Life Insurance?

The price of your policy depends on several things:

| Factor | Impact on Cost |

|---|---|

| Age | Lower if younger |

| Health | Lower if healthy |

| Smoking | Much higher if you smoke |

| Coverage Amount | Higher for larger policies |

| Policy Length | Longer terms cost more |

| Gender | Usually lower for women |

| Hobbies/Jobs | Higher for risky activities |

Two Insights Many Miss

- Even a small health issue can change your rate. For example, high blood pressure or being overweight may raise your price, even if you feel healthy.

- Smokers pay much more—sometimes double or triple the cost for the same coverage. If you quit smoking for a year or more, you may qualify for lower rates.

How To Find The Most Affordable Policy

Buying affordable life insurance takes more than just picking the lowest price. Here are smart steps to get the best deal:

- Compare quotes from several companies. Prices can vary a lot for the same person.

- Choose the right coverage amount and term. Don’t buy more than you need.

- Buy when you’re young and healthy. Prices go up every year you wait.

- Ask about discounts. Some companies give lower rates if you’re very healthy or buy online.

- Check the insurance company’s ratings. You want a company that will be there when your family needs them.

Real-world Example

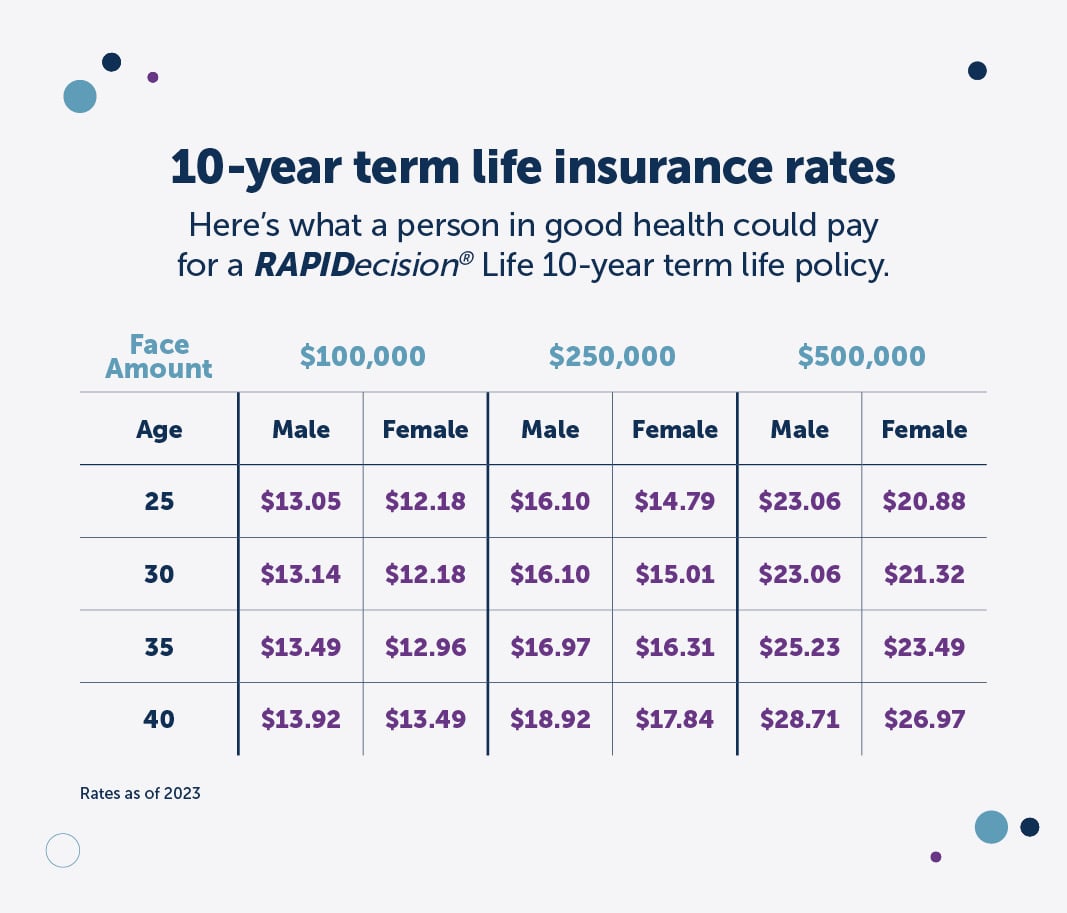

A healthy 30-year-old non-smoker can buy a $500,000, 20-year term policy for about $20–$25 per month. A 45-year-old with the same health might pay $50–$60 per month for the same coverage.

Comparing Top Life Insurance Companies For Affordability

Let’s look at a simple comparison of sample monthly costs for a healthy 30-year-old, non-smoker buying a $250,000, 20-year term policy.

| Company | Monthly Cost | Customer Service Rating | Application Speed |

|---|---|---|---|

| Haven Life | $13 | Excellent | Fast (online) |

| Banner Life | $14 | Very Good | Medium |

| State Farm | $15 | Excellent | Medium |

| Protective | $13 | Good | Fast |

| Prudential | $16 | Very Good | Slow |

Tip: The lowest price is not always the best choice. Look at customer service and how easy it is to file a claim.

Common Mistakes When Buying Affordable Life Insurance

Many people new to life insurance make the same mistakes. Avoid these to get the best value:

- Choosing the cheapest policy only: Low price is important, but make sure the company is reliable and the coverage is enough.

- Waiting too long: Prices go up as you age or if your health changes.

- Not reviewing your needs: Your insurance should change as your life changes (marriage, kids, new home).

- Forgetting inflation: Costs go up over time. Make sure your coverage is enough for future expenses.

- Not telling the truth on your application: Giving wrong information can void your policy.

Is It Ever A Bad Idea To Buy The Cheapest Policy?

It can be. Sometimes, very cheap policies have:

- Low coverage amounts that will not help your family much.

- Limited benefits (no payout for certain causes of death).

- Unreliable companies that make it hard for your family to get the money.

Always check the insurance company’s reputation and read the details before buying.

How To Save Even More On Life Insurance

- Improve your health: Lower blood pressure, lose weight, and stop smoking before you apply.

- Pay annually: Some companies offer discounts if you pay once a year instead of monthly.

- Bundle policies: If you buy other insurance (like home or auto) from the same company, ask for a discount.

- Review your policy every few years: As your life changes, you may be able to reduce coverage and save money.

When To Skip Life Insurance

Not everyone needs life insurance. You may not need a policy if:

- No one depends on your income

- You have enough savings to cover your debts and funeral costs

- Your children are grown and financially independent

Still, life insurance is a simple way to give your loved ones peace of mind.

Where To Learn More

If you want more details, the National Association of Insurance Commissioners offers guides and tools for consumers. Visit their website at NAIC Consumer Information.

Frequently Asked Questions

What Is The Cheapest Type Of Life Insurance?

Term life insurance is usually the cheapest. It gives coverage for a set number of years, with no cash value or investment part. Whole life and other permanent policies cost much more.

Can I Get Affordable Life Insurance With Health Problems?

Yes, but it may cost more. Some companies offer no-exam or guaranteed issue policies, but these are usually more expensive. Improving your health before you apply can help lower your cost.

How Can I Lower My Life Insurance Premium?

- Buy when you are young and healthy

- Improve your health (stop smoking, exercise)

- Compare quotes from different companies

- Choose a shorter term or lower coverage if possible

Does Affordable Life Insurance Cover Covid-19 Or Pandemics?

Most term life insurance policies cover death from COVID-19 and other illnesses. Check the policy details to be sure, as exclusions are rare but possible.

Can I Change My Life Insurance Policy If My Needs Change?

Yes. You can usually cancel, increase, or decrease your coverage, or even switch to a new policy. Review your needs every few years to make sure you have the right amount of insurance.

Choosing the right affordable life insurance policy is one of the smartest ways to protect your family’s future. It doesn’t need to be expensive or complicated. By understanding your needs, comparing options, and avoiding common mistakes, you can find a policy that gives peace of mind—without straining your budget.

Read More:

- Business Liability Insurance Quote: Get the Best Rates Today

- Private Health Insurance Plans: Top Benefits and How to Choose

- Best Car Insurance Quotes Online: Save Big With Top Rates

- Compare Home Insurance Rates: Save Money With Smart Choices

- Best Personal Loan Rates: Unlock Top Offers for 2024

- Small Business Loan Pre Approval: Unlock Funding Faster

- Debt Consolidation Loan Online: Simplify Your Finances Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today