Private Health Insurance Plans: A Complete Guide For Smart Choices

Many people worry about health care costs. If you live in the US or another country without universal health care, you may want more control over your health expenses. Private health insurance plans can give you this control. They help you pay for medical bills, offer extra services, and sometimes let you see more doctors.

But choosing a plan is not simple. There are many options, rules, and hidden costs. This guide explains private health insurance plans clearly, with practical advice, real data, and examples. You’ll learn how these plans work, how to compare them, and how to avoid common mistakes.

What Is Private Health Insurance?

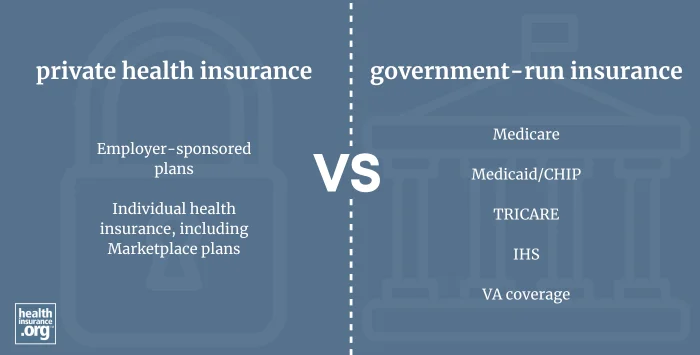

Private health insurance is coverage offered by non-government companies. You pay a monthly fee (called a premium) and the company pays part of your medical expenses. Private insurance can cover doctor visits, hospital stays, medicines, surgeries, and more.

Some people buy their own plan. Others get coverage through their employer. Private plans are different from government programs like Medicare or Medicaid. If you want more choice or better service, private insurance may be the right option.

Types Of Private Health Insurance Plans

There are several main types of private health insurance plans. Each has its own rules, costs, and benefits.

Health Maintenance Organization (hmo)

HMO plans are usually cheaper. You must use doctors and hospitals in the plan’s network. You need a primary care doctor who must refer you to specialists.

Preferred Provider Organization (ppo)

PPO plans are more flexible. You can visit any doctor, but you pay less for doctors in the network. You don’t need referrals to see specialists.

Exclusive Provider Organization (epo)

EPO plans only cover care from network providers. They don’t require referrals, but you pay the full cost if you go outside the network.

Point Of Service (pos)

POS plans combine HMO and PPO features. You need a primary doctor and referrals, but can visit out-of-network providers at a higher cost.

High-deductible Health Plan (hdhp)

HDHPs have lower premiums, but you pay more out-of-pocket before the plan covers costs. These are often paired with Health Savings Accounts (HSA).

Key Features To Compare

Choosing a private health insurance plan is not just about price. You must look at several important features.

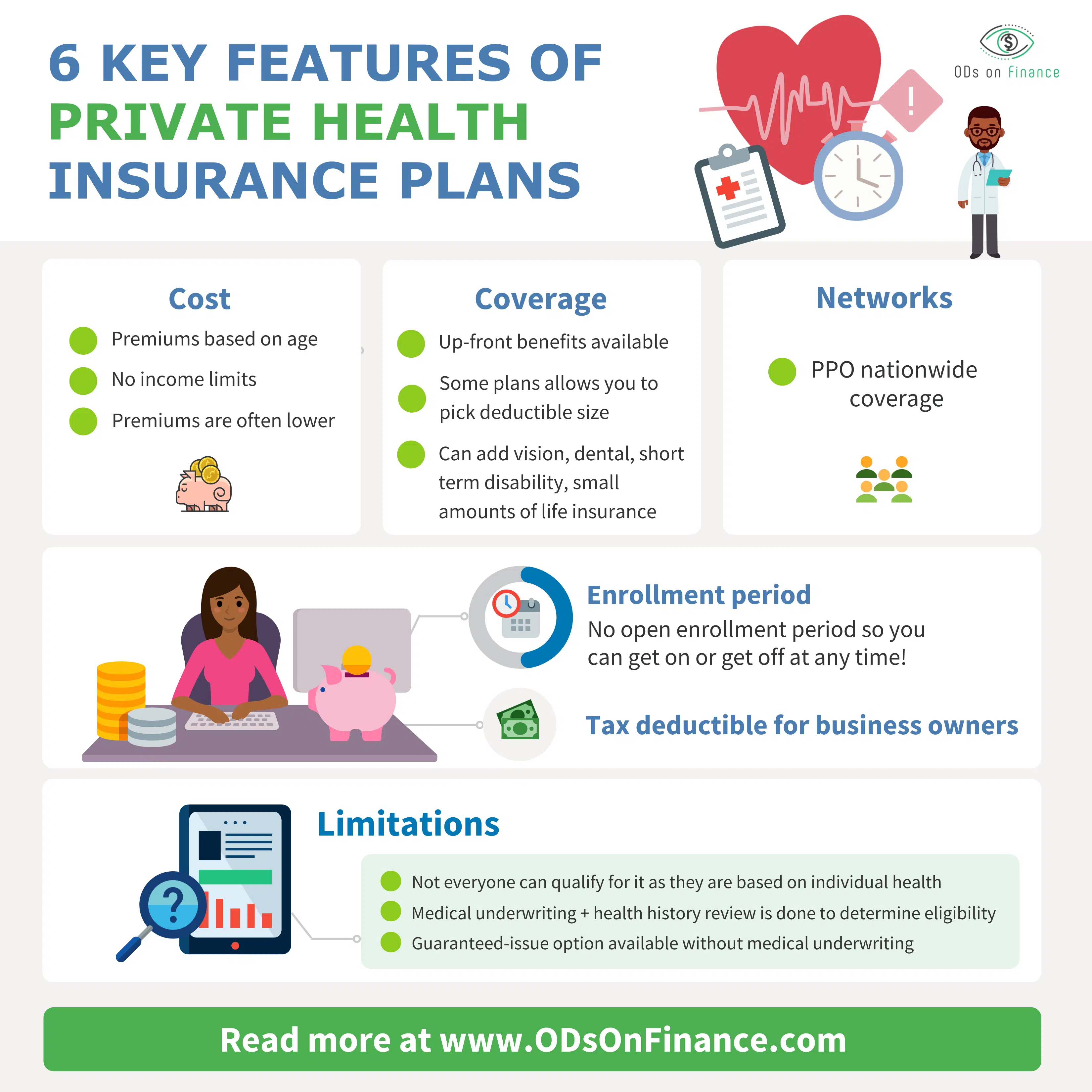

Premiums

This is the monthly fee you pay. Lower premiums can mean higher out-of-pocket costs later.

Deductibles

The deductible is the amount you pay before insurance starts paying. High deductibles mean you pay more yourself at first.

Copayments And Coinsurance

A copayment is a fixed fee for each visit or medicine. Coinsurance is a percentage you pay after reaching your deductible.

Network Providers

Most plans have a network of doctors and hospitals. Out-of-network care is often more expensive or not covered.

Coverage Limits

Some plans have limits on certain services, like therapy or prescription drugs.

Out-of-pocket Maximums

This is the most you pay in a year for covered services. After this, the plan pays 100%.

Comparing Private Health Insurance Plans

It’s helpful to see how different plans compare. Here is a sample comparison:

| Plan Type | Average Premium | Deductible | Network Flexibility | Referral Needed? |

|---|---|---|---|---|

| HMO | $450/month | $1,500 | Limited | Yes |

| PPO | $550/month | $1,000 | High | No |

| EPO | $500/month | $1,200 | Moderate | No |

| POS | $475/month | $1,300 | Moderate | Yes |

| HDHP | $350/month | $3,000 | High | No |

You can see that HDHPs have the lowest premiums but much higher deductibles. PPOs cost more but offer the most flexibility.

Common Mistakes When Choosing A Plan

Many people make mistakes when picking a private health insurance plan. Here are some you should avoid:

- Ignoring the network: Some plans have small networks. If your doctor or hospital is not included, you may pay more or lose access.

- Focusing only on premiums: Low premiums can mean high deductibles or bad coverage.

- Not checking coverage details: Some plans limit prescription drugs, mental health, or special treatments.

- Forgetting out-of-pocket maximums: This is the most you pay in a year. A low maximum can protect you from large bills.

- Missing enrollment deadlines: Private plans often have strict enrollment periods.

Who Should Consider Private Health Insurance?

Private health insurance is best for people who:

- Don’t qualify for government plans.

- Want more choice in doctors or hospitals.

- Need coverage for special treatments.

- Travel often and need flexible care.

Some people also buy private insurance as secondary coverage. For example, if you have Medicare, you can add a private plan for extra benefits.

Cost Trends And Data

Health insurance costs are rising. In 2023, the average annual premium for employer-sponsored family coverage in the US was $23,968. For single coverage, it was $8,435. These numbers are up 7% from the previous year.

Deductibles have also increased. The average deductible for single coverage is now $1,735. Some plans have deductibles over $3,000.

Here is a table showing premium growth over recent years:

| Year | Family Premium | Single Premium | % Change |

|---|---|---|---|

| 2020 | $21,342 | $7,581 | +5% |

| 2021 | $22,221 | $7,739 | +4% |

| 2022 | $22,463 | $8,003 | +3% |

| 2023 | $23,968 | $8,435 | +7% |

This steady increase is important to consider when budgeting for health insurance.

What Affects Your Insurance Cost?

Several factors influence your cost:

- Age: Older people pay higher premiums.

- Location: Costs vary by state and city.

- Plan Type: More flexible plans cost more.

- Coverage Level: More coverage means higher premiums.

- Health Status: Some plans may charge more for pre-existing conditions.

- Family Size: Adding family members increases cost.

Here is an example of how age affects premium costs:

| Age | Average Monthly Premium |

|---|---|

| 25 | $320 |

| 35 | $370 |

| 45 | $480 |

| 55 | $620 |

| 65 | $740 |

Non-obvious Insights And Tips

Some facts about private health insurance are not obvious to beginners:

- Plans often change networks and coverage every year. Always check the new policy before renewing.

- Many plans have hidden fees, like facility charges or out-of-network lab costs. Ask for a complete summary of benefits before enrolling.

- Choosing a high-deductible plan can save money if you are healthy, but may be risky if you need regular care.

- Some private plans offer wellness rewards. You can earn discounts for healthy habits or checkups.

- Not all medicines are covered. Check the formulary (drug list) to make sure your needed medications are included.

How To Shop For Private Health Insurance

If you are buying your own plan, follow these steps:

- Check eligibility: Some plans are only for certain age groups or jobs.

- Compare plans: Use online tools and company websites to compare premiums, deductibles, and coverage.

- Read the fine print: Look for exclusions, coverage limits, and network lists.

- Estimate your health needs: Think about how often you visit doctors, use prescriptions, or need special care.

- Ask for help: Insurance brokers can explain details and help you choose the best plan.

- Review every year: Plans and prices change. Make sure your plan still fits your needs.

Real-life Example

Maria is 40 years old and needs coverage for her family. She considers an HMO and a PPO. The HMO is cheaper, but her child’s doctor is not in the network. The PPO costs more, but covers her child’s doctor and nearby hospitals.

Maria chooses the PPO because she values flexibility. She also checks the out-of-pocket maximum to make sure she won’t face huge bills if someone gets sick.

Additional Benefits Of Private Health Insurance

Private health insurance plans often offer extra services:

- Telehealth: Online doctor visits.

- Dental and vision: Some plans include these or offer them as add-ons.

- Wellness programs: Discounts on gym memberships or health coaching.

- Travel coverage: Emergency care when traveling outside your home area.

Some plans also include mental health services, which are becoming more important. Always check for these extras when comparing plans.

How To Use Your Insurance Wisely

Once you have a plan, keep these tips in mind:

- Stay in-network to save money.

- Keep records of all medical bills and insurance statements.

- Use preventive care (like annual checkups), which is often free.

- Contact customer service if you have questions or problems.

- Review your coverage yearly and update if your health needs change.

Frequently Asked Questions

What Is The Difference Between Private And Public Health Insurance?

Private health insurance is offered by companies and lets you choose your plan, doctor, and coverage. Public health insurance (like Medicare or Medicaid) is run by the government and often has more rules and less choice.

Can I Buy Private Health Insurance If I Have A Pre-existing Condition?

Yes, in the US and many countries, you can buy private insurance even if you have pre-existing conditions. Some plans may cost more, but they cannot refuse you.

How Do I Find Out If My Doctor Is In-network?

Ask your doctor’s office or check the insurance company’s website. Networks change often, so check every year.

Are Prescription Drugs Covered By Private Insurance?

Most private plans cover some prescription drugs, but not all. Check the formulary before enrolling to see if your medications are included.

Can I Change My Private Health Insurance Plan Anytime?

Usually, you can only change plans during open enrollment or if you have a qualifying life event (like marriage, birth, or job change). Check the rules for your area.

Private health insurance plans are a smart way to manage your health care costs and choices. By learning about plan types, comparing features, and asking the right questions, you can find a plan that fits your needs and budget. Remember to read all details, check coverage every year, and use your plan wisely. If you want more detailed data about health insurance trends, visit KFF Health Costs Survey for the latest research and facts. Your health and finances deserve careful planning, so take your time and make an informed decision.

Read More:

- Affordable Life Insurance Policy: Secure Your Future Without Breaking the Bank

- Business Liability Insurance Quote: Get the Best Rates Today

- Best Car Insurance Quotes Online: Save Big With Top Rates

- Compare Home Insurance Rates: Save Money With Smart Choices

- Best Personal Loan Rates: Unlock Top Offers for 2024

- Small Business Loan Pre Approval: Unlock Funding Faster

- Debt Consolidation Loan Online: Simplify Your Finances Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today