When you buy life insurance, you expect your family will receive financial help when you’re gone. But sometimes, insurance companies deny claims, leaving loved ones confused and worried. In these moments, a life insurance claim denial lawyer becomes essential. Understanding when and why these claims get denied, and how a lawyer can help, can make all the difference. This guide explains the process, common reasons for denial, how to respond, and the critical role a lawyer plays in getting your family the support they deserve.

Why Life Insurance Claims Get Denied

Insurance companies do not deny every claim. But when they do, it’s often for specific reasons. Here are some of the most common:

- Non-disclosure or misrepresentation: The insurer claims the policyholder hid important health information or lied on the application.

- Policy lapse: Premiums were not paid, so the policy was no longer active at the time of death.

- Contestability period: If the policyholder dies within the first two years, the insurer reviews the application closely for errors or lies.

- Excluded causes of death: Some policies exclude suicide, dangerous activities, or certain illnesses.

- Incorrect beneficiary details: Disputes or errors with the named beneficiary can delay or stop payouts.

- Fraud or suspicious circumstances: The insurer suspects fraud or unclear circumstances around the death.

Real-world Example

For instance, a father buys a $500,000 life insurance policy. He forgets to mention a heart condition. He passes away one year later. The insurer finds this omission during the contestability period and denies the claim, stating misrepresentation.

The Insurance Company’s Perspective

Insurance companies are businesses. They protect themselves from losses by investigating claims for possible errors or fraud. Sometimes, even honest mistakes can lead to denial. While some denials are justified, others are not. Insurers rely on policy language, medical records, and legal technicalities.

Understanding their process helps you respond more effectively.

Your Rights As A Beneficiary

As a beneficiary, you have legal rights. The insurance company must:

- Provide written reasons for denial.

- Share the evidence or documents used in their decision.

- Allow you to appeal or contest the denial.

You can request policy documents, correspondence, and the claim file. If the insurer refuses, a lawyer can demand these records on your behalf.

What Does A Life Insurance Claim Denial Lawyer Do?

A life insurance claim denial lawyer is a legal professional who helps beneficiaries challenge denied claims. Their main jobs include:

- Reviewing the denial letter and policy details.

- Gathering evidence, such as medical records and application forms.

- Communicating with the insurance company.

- Filing appeals or lawsuits if necessary.

- Negotiating settlements.

They know insurance law and how to fight for your rights. Without expert help, many people accept the denial or miss important deadlines.

When Should You Hire A Lawyer?

Not every denied claim needs a lawyer. But you should strongly consider hiring one if:

- The reason for denial is unclear or seems unfair.

- The insurer claims fraud or misrepresentation.

- The policy language is confusing.

- The amount at stake is large.

- You have tried to appeal but were unsuccessful.

A lawyer’s early involvement can prevent costly mistakes and increase your chances of getting paid.

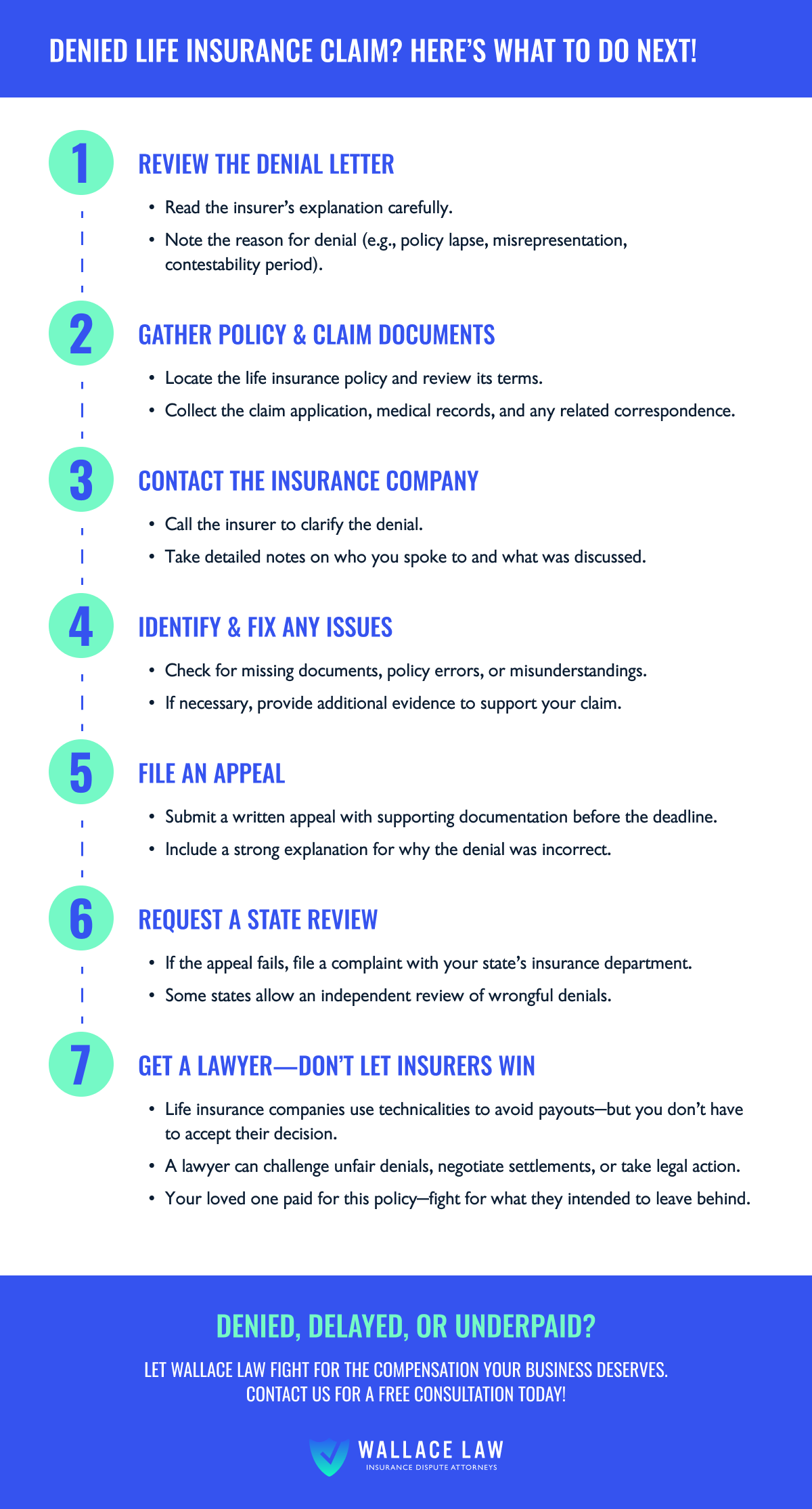

The Claim Denial Appeal Process

Step 1: Read The Denial Letter

Start by reading the denial letter carefully. It explains the insurance company’s reasons. Check if their explanation matches the facts.

Step 2: Collect Evidence

Gather all policy documents, payment records, medical reports, and communication with the insurer. Strong evidence is key to a successful appeal.

Step 3: Appeal Directly

Send a written appeal to the insurer. Clearly explain why you believe the denial is wrong. Include supporting documents.

Step 4: Seek Legal Help

If the insurer refuses your appeal, contact a life insurance claim denial lawyer. They can review your case and recommend next steps, including legal action.

Typical Timeline

Claim denials and appeals can take weeks or months. In some cases, legal action may take over a year. Patience and persistence are important.

Comparing Diy Appeals Vs. Lawyer-assisted Appeals

Here’s a comparison of handling a denied claim yourself versus hiring a lawyer:

| Factor | DIY Appeal | With Lawyer |

|---|---|---|

| Success Rate | Lower, especially if complex | Higher, due to experience |

| Time Required | High (self-managed) | Lawyer handles process |

| Legal Knowledge Needed | Must learn insurance law | Lawyer already trained |

| Cost | Usually free, but risky | Fees apply, but often “no win, no fee” |

| Stress Level | High | Lower |

Key Qualities Of A Good Life Insurance Claim Denial Lawyer

Not all lawyers are the same. Look for these qualities:

- Experience with life insurance cases

- Clear communication skills

- Proven track record of successful appeals

- Transparent fees (many work on contingency)

- Strong negotiation skills

Ask for references or case examples before hiring.

Common Pitfalls In Life Insurance Claim Appeals

Many people make mistakes when appealing a denied claim. Here are common pitfalls to avoid:

- Missing deadlines: Insurance policies and states set strict time limits for appeals.

- Incomplete documentation: Missing documents weaken your case.

- Emotional responses: Stay focused on facts, not feelings.

- Not consulting a lawyer: Some denials need legal expertise.

- Ignoring small details: Even minor errors in names, dates, or policy numbers can cause problems.

How Much Does A Life Insurance Claim Denial Lawyer Cost?

Most lawyers in this field use a contingency fee. This means you pay nothing unless you win. Typical fees range from 25% to 40% of the payout. Some may charge hourly or flat fees, especially for simple advice.

| Fee Type | When Paid | Typical Percentage/Amount |

|---|---|---|

| Contingency Fee | After winning | 25%–40% of payout |

| Hourly Fee | As work is done | $200–$500/hour |

| Flat Fee | Upfront or after service | $1,000–$5,000 |

Before hiring, ask for a written fee agreement.

Examples Of Successful Claim Denial Appeals

- A widow’s claim was denied due to a “technical error” in the policy. Her lawyer proved the deceased intended to name her as beneficiary. The insurer paid out after legal pressure.

- A claim was rejected for alleged misrepresentation about smoking. The lawyer provided medical evidence showing the policyholder had quit years earlier. The insurer reversed the denial.

- A family faced denial after the policy lapsed by one week. The lawyer showed payment delays were due to the insurer’s system error. The claim was paid.

These examples show the value of legal expertise.

What Documents Does Your Lawyer Need?

To build a strong case, your lawyer will ask for:

- The policy document: Shows terms, exclusions, and coverage.

- Denial letter: States the insurer’s reasons for denying.

- Medical records: If health issues are in question.

- Payment history: Proves premiums were paid.

- Death certificate: Confirms date and cause of death.

- All communication with the insurer.

Organize these documents early to speed up your case.

Non-obvious Insights Most People Miss

- Policy updates matter: Even small changes, like updating your address or beneficiary, should be confirmed in writing. Insurers may deny claims based on outdated records.

- State laws differ: Each state has unique insurance rules. A local lawyer knows how to use these laws to your advantage.

- Independent medical reviews: Sometimes, you can request an outside medical review if the insurer claims your loved one’s death was excluded by the policy.

- Group vs. individual policies: Group life insurance (through work) may have different rules and appeal processes than private policies.

- Rescission risk: If the insurer claims fraud, they may try to “rescind” (cancel) the policy entirely, not just deny the claim. Legal help is critical in these cases.

How To Avoid Claim Denial In The Future

While you cannot control every factor, you can reduce the chance of denial by:

- Filling out applications honestly and completely.

- Updating beneficiaries after life changes (marriage, divorce, birth).

- Paying premiums on time.

- Keeping copies of all documents and payments.

- Reading the policy and asking questions about unclear terms.

These steps protect your family and make future claims smoother.

How To Choose The Right Lawyer For Your Case

With so many lawyers available, finding the right fit is important. Here’s what to consider:

- Specialization: Choose someone who focuses on life insurance, not just general law.

- Location: Local lawyers know state-specific rules.

- Reputation: Check reviews and ask for past client feedback.

- Fee structure: Understand costs before signing.

- Communication: Pick a lawyer who explains things clearly and answers your questions.

Schedule an initial consultation and trust your instincts.

External Resource

For more information about insurance law and claim denials, visit the National Association of Insurance Commissioners.

Frequently Asked Questions

What Should I Do First If My Life Insurance Claim Is Denied?

Start by reading the denial letter carefully. Look for the specific reason for denial. Gather all your policy documents and any correspondence with the insurer. Then, consider contacting a life insurance claim denial lawyer to review your case and discuss possible next steps.

How Long Do I Have To Appeal A Denied Claim?

Most insurance companies set a deadline, usually 60 to 180 days, for appeals. Some states also set their own limits. Missing the deadline can end your right to appeal, so act quickly.

How Can A Lawyer Help If I Already Appealed And Was Denied Again?

A lawyer can review your entire case, spot errors or unfair practices, and take legal action. This might include filing a lawsuit, negotiating with the insurer, or using state insurance regulators to force a review.

What Does “contestability Period” Mean In A Life Insurance Policy?

The contestability period is typically the first two years after you buy a policy. If the insured person dies during this time, the insurer can review the application for errors, misstatements, or omissions. If they find something, they may deny the claim or adjust the payout.

Will Hiring A Lawyer Guarantee My Life Insurance Claim Is Paid?

No lawyer can guarantee a result, but a skilled life insurance claim denial lawyer improves your chances. They understand the law, know how insurers operate, and can often find solutions you might miss.

Getting a life insurance claim denied feels overwhelming, especially during a time of loss. But you don’t have to face it alone. With the right legal help and information, you can challenge unfair denials and protect your family’s future. Take action quickly, stay organized, and don’t be afraid to seek expert guidance.

Your loved one’s legacy is worth fighting for.

Read More:

- Affordable Life Insurance Policy: Secure Your Future Without Breaking the Bank

- Business Liability Insurance Quote: Get the Best Rates Today

- Private Health Insurance Plans: Top Benefits and How to Choose

- Best Car Insurance Quotes Online: Save Big With Top Rates

- Compare Home Insurance Rates: Save Money With Smart Choices

- Best Personal Loan Rates: Unlock Top Offers for 2024

- Small Business Loan Pre Approval: Unlock Funding Faster

- Debt Consolidation Loan Online: Simplify Your Finances Today