Car accidents are stressful events that often leave people worried about their health, their vehicles, and their finances. If you have car insurance, filing a claim is the next step to get compensation for damages or injuries. But many drivers do not understand how the car accident insurance claim settlement process works, what to expect, or how to avoid mistakes. This guide gives you clear, practical advice about settling your claim smoothly, so you can focus on recovery rather than paperwork.

Understanding Car Accident Insurance Claims

A car accident insurance claim is a request you make to your insurance company after an accident. You ask them to pay for repairs, medical bills, or other costs covered by your policy. The process begins as soon as you report the incident.

How your claim is settled depends on the type of coverage, the accident details, and the insurance company’s rules.

There are two main types of claims:

- First-party claims: You file with your own insurer.

- Third-party claims: You file with another driver’s insurer if they caused the accident.

Most people deal with first-party claims unless the accident is clearly someone else’s fault.

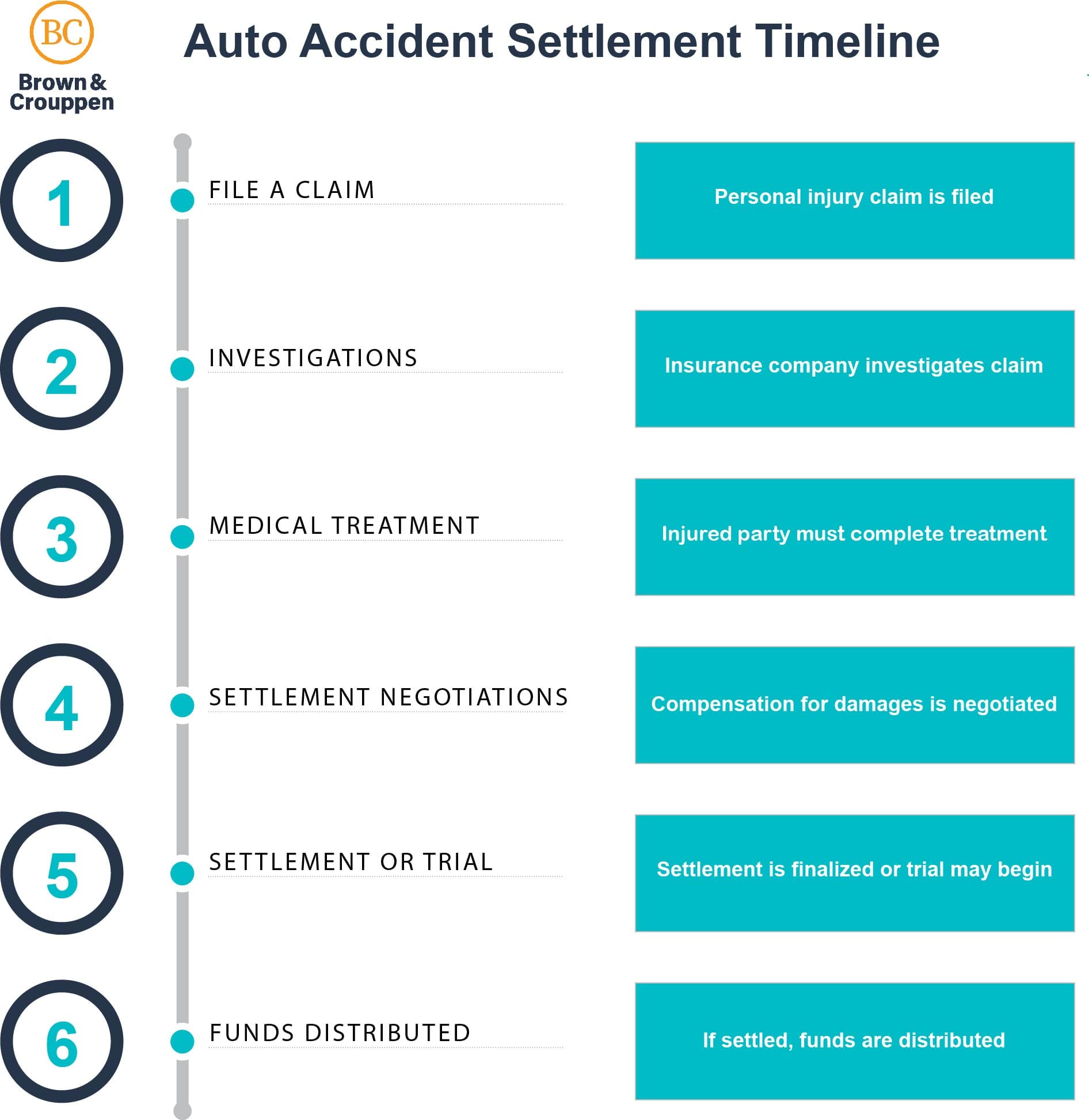

Steps To File A Car Accident Insurance Claim

Getting your claim settled starts with following the right steps. Missing details or mistakes can delay your settlement or reduce your payout.

- Report the Accident: Contact your insurer as soon as possible, ideally within 24 hours. Provide basic information about the accident and any injuries.

- Collect Evidence: Take photos of the scene, your car, the other vehicles, and any injuries. Gather police reports, witness statements, and receipts.

- Fill Out Claim Forms: Your insurer will ask you to complete forms describing what happened. Be honest and accurate.

- Meet with the Adjuster: The insurance company sends an adjuster to inspect your vehicle and review damages. They may also ask questions about the accident.

- Get Repair Estimates: You can get quotes from repair shops. Sometimes your insurer will suggest certain shops.

- Review the Settlement Offer: The insurer will propose a payment based on their assessment. You can accept, negotiate, or reject it.

- Receive Payment: Once you agree, the insurer pays you or the repair shop. If injuries are involved, medical bills may be paid directly.

Not every claim follows this exact order, but these steps cover most situations.

What Affects Your Claim Settlement?

Several factors decide how much you receive from your claim. Understanding these helps you avoid surprises.

Policy Coverage

Your car insurance policy sets limits on what is covered. Common types include:

- Liability: Covers damage/injury you cause to others.

- Collision: Covers your car’s damage, regardless of fault.

- Comprehensive: Covers non-collision events like theft or weather.

- Medical payments: Covers medical costs for you and passengers.

If your policy has low limits or high deductibles, your payout will be smaller.

Fault Determination

Insurance companies decide who caused the accident. If you are found at fault, your claim may be reduced or denied. In some states, like California, fault can be split between drivers, affecting payouts.

Damage Assessment

Insurers use adjusters to inspect your car, review reports, and estimate repair costs. Sometimes they offer less than what a repair shop quotes. You can negotiate or request another assessment.

Documentation Quality

Claims with clear photos, accurate reports, and medical records are settled faster and for higher amounts. Missing or unclear evidence can delay your claim or lower your payout.

State Laws

Every state has different rules about insurance claims. For example, some have “no-fault” laws where your own insurer pays, no matter who caused the accident. Others require you to prove fault.

Common Mistakes That Delay Settlement

Even experienced drivers make mistakes that slow down or hurt their claim. Here are errors to avoid:

- Not Reporting Quickly: Waiting too long may lead to denial.

- Incomplete Evidence: Missing photos or documents weakens your claim.

- Admitting Fault Too Soon: Let insurers and police decide fault.

- Ignoring Medical Care: Not seeing a doctor after an accident can reduce injury payouts.

- Accepting First Offer: Sometimes initial offers are too low. Negotiate if you think repairs or medical costs are higher.

Many beginners forget to review their policy before filing a claim, which can lead to confusion or disappointment. Also, do not ignore emails or calls from the insurer—prompt replies help your claim move faster.

Comparing Insurance Claim Settlement Speeds

Insurance companies vary in how fast they settle claims. Here is a comparison of average settlement times for major US insurers:

| Insurance Company | Average Settlement Time | Customer Satisfaction (1–5) |

|---|---|---|

| State Farm | 10–30 days | 4.5 |

| Geico | 8–25 days | 4.4 |

| Progressive | 12–35 days | 4.2 |

| Allstate | 14–40 days | 4.0 |

If your claim involves injuries or complex damages, it may take longer. Some claims, especially those with legal issues, can take several months.

Negotiating Your Settlement

You do not have to accept the first offer from your insurer. Negotiation is common, especially if you feel the payment does not cover your losses.

How To Negotiate

- Review the Offer: Check if the amount covers repairs, medical costs, and other expenses.

- Collect Independent Estimates: Get quotes from other repair shops or doctors.

- Write a Response: Explain why you believe the offer is too low. Use evidence like receipts, photos, and reports.

- Stay Polite but Firm: Insurers respond better to calm, factual communication.

- Consider Legal Help: If you are stuck, a lawyer can help, especially in injury cases.

Most people do not realize you can ask for a “diminished value” payment if your car loses resale value after repairs. This is a non-obvious insight that can increase your settlement.

How Insurance Companies Calculate Settlements

Insurers use formulas and data to decide your payout. Here is a simple example of how they calculate repair costs:

| Repair Item | Estimated Cost | Deductible | Final Payout |

|---|---|---|---|

| Bumper Replacement | $800 | $500 | $300 |

| Paint Work | $600 | $500 | $100 |

| Wheel Alignment | $200 | $500 | $0 |

If your deductible is higher than the repair cost, you may not get a payout. Always check your policy’s deductible before filing a claim.

Real-life Example Of Claim Settlement

Let’s look at a typical case:

Maria’s car was hit by another driver at a stoplight. She reported the accident, collected photos, and got a police report. Her insurer sent an adjuster who estimated $2,000 in damages. Maria got quotes from two repair shops—one was $2,500, the other $1,900.

She submitted both quotes. The insurer offered $1,900 minus her $500 deductible, so Maria received $1,400.

Maria noticed her car lost value after repairs. She requested a diminished value claim and got an extra $600. Many people miss this extra payout unless they ask.

Settling Claims Involving Injuries

Claims for injuries are more complex. Insurers review medical reports, bills, and sometimes ask for independent medical exams. Settlements may include:

- Emergency care costs

- Ongoing treatment

- Lost wages if you miss work

- Pain and suffering (in some cases)

If injuries are serious, you may need a lawyer to help negotiate. Settlement amounts can range from a few hundred to hundreds of thousands of dollars, depending on severity.

Data On Claim Settlement Amounts

Here is a comparison of average settlement amounts in the US for property damage and injury claims:

| Claim Type | Average Settlement | Range |

|---|---|---|

| Property Damage | $3,231 | $1,000–$7,000 |

| Bodily Injury | $17,000 | $1,500–$75,000 |

These numbers are averages; your payout may be higher or lower based on your case.

Tips For A Smooth Claim Settlement

Getting your claim settled faster and for the best amount takes planning and attention to detail. Here are some practical tips:

- Keep Good Records: Save all documents, photos, and receipts.

- Communicate Clearly: Reply to insurer requests quickly.

- Know Your Policy: Understand coverage, deductibles, and limits before filing.

- Stay Honest: Giving false information can get your claim denied.

- Ask About Extra Payments: Like diminished value or rental car coverage.

A non-obvious insight: Many policies cover rental cars while yours is being repaired, but you must request this benefit. Always ask your insurer what else is covered.

When To Get Legal Help

You may need a lawyer if:

- Injuries are serious or long-term

- The other driver disputes fault

- The insurer denies your claim or offers too little

- You face legal deadlines or complex paperwork

Legal help can increase your settlement, especially for injury cases. However, lawyers take a percentage of your payout, so weigh the costs.

How Long Should Settlement Take?

Most simple claims settle in 10–30 days. Injury claims or disputes may take months. If your claim takes longer, ask your insurer for updates and reasons for the delay.

If you want more information about insurance claims and settlements, visit Insurance Information Institute for expert advice.

Frequently Asked Questions

What Documents Do I Need To File A Car Accident Insurance Claim?

You need photos of the accident, the police report, your insurance policy number, repair shop estimates, and any medical records if injuries are involved.

How Is Fault Determined In A Car Accident?

Insurance companies use police reports, witness statements, and vehicle damage to decide who caused the accident. In some states, fault can be split between drivers, affecting payouts.

Can I Negotiate The Settlement Offer From My Insurer?

Yes, you can negotiate. Use repair shop quotes, medical bills, and evidence to support your claim if you believe the offer is too low.

What Happens If The Other Driver Is Uninsured?

If the other driver is uninsured, your own uninsured motorist coverage (if you have it) may pay for your damages. Otherwise, you may need to pay out of pocket or take legal action.

How Long Does The Claim Settlement Process Usually Take?

Most property damage claims settle in 10–30 days. Injury claims or complex cases can take several months. Always ask your insurer for updates if your claim is delayed.

Getting a car accident insurance claim settled can feel overwhelming, but understanding the process, avoiding mistakes, and staying organized will help you get the payout you deserve. Remember to review your policy, collect strong evidence, and communicate clearly with your insurer.

If things get complicated, do not hesitate to seek professional help. A successful claim means less stress and a faster return to normal life.

Read More:

- Affordable Life Insurance Policy: Secure Your Future Without Breaking the Bank

- Business Liability Insurance Quote: Get the Best Rates Today

- Private Health Insurance Plans: Top Benefits and How to Choose

- Best Car Insurance Quotes Online: Save Big With Top Rates

- Compare Home Insurance Rates: Save Money With Smart Choices

- Best Personal Loan Rates: Unlock Top Offers for 2024

- Small Business Loan Pre Approval: Unlock Funding Faster

- Debt Consolidation Loan Online: Simplify Your Finances Today